Next-Gen Best Trading Platform at Your Fingertips

Built for Traders:

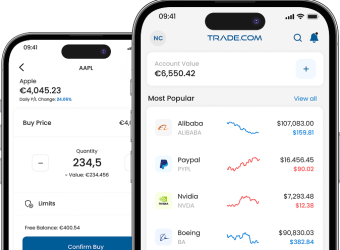

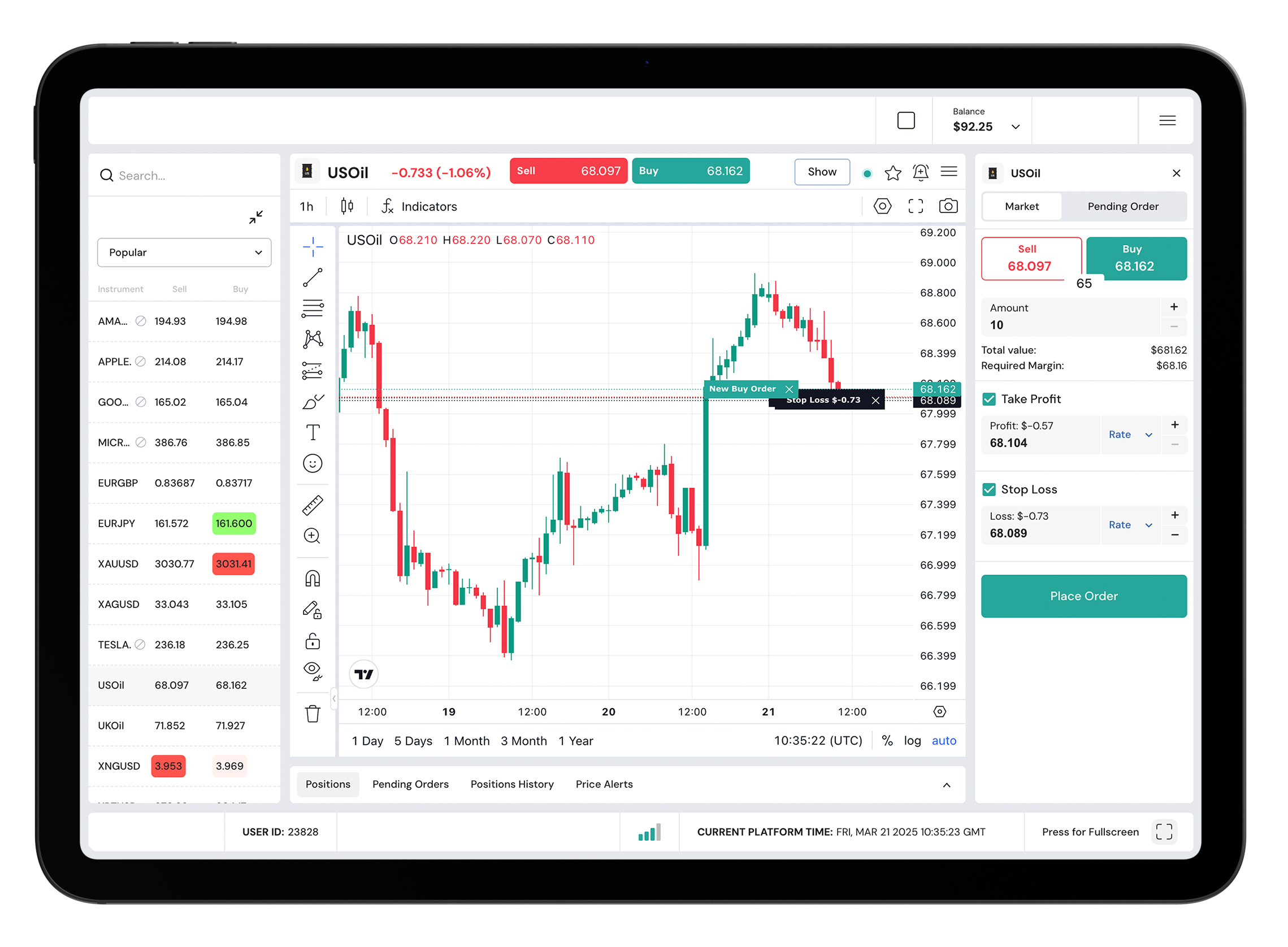

A Seamless Online Trading Platform

Access Global Trading Markets

Trade 1200+ instruments, including stocks, forex, indices, and ETFs — all with a single login.

Benefit from Low Spreads

Enjoy spreads from 0.3 pip. Keep more of your profits with faster, more efficient trading.

24/5 Dedicated Trade Support

Get real-time expert help. Our 24/5 trading support is here when it matters most.

Safe and Regulated Online Trading

Your funds are protected by secure and, continuously monitored trading systems.

Why let devices hold back your Trading Experience?

Build your trading strategy and track market trends, effortlessly

AI driven trading

Boost your investment returns with powerful, innovative, AI-driven trading tools—intelligently designed to analyse markets, spot opportunities, and think ahead to help you trade better.

Trade with confidence

With Trade’s expert insights, smart alerts tailored to your strategy, and professional-grade charting tools, you’ll trade with confidence and clarity.

Personal market analyst

Whether you’re spotting trends or timing your exits, it’s like having a personal market analyst by your side — 24/7.

*The Company reserves the right to widen spreads, decrease leverage, increase margin requirements, control maximum order amounts and limit clients’ total exposure. In order to see the current overnight rollovers for instruments traded on WebTrader, click on the instrument on the table above. For MT5 please click here.

** Quotes are delayed

*** The above prices are only for indicative purposes

Money and Assets protection

Commodity Trading for Beginners

1. What is Forex? Trade.com experts explain this for beginners.

Know more!

2. How to manage your trading risk while trading in forex?

Know more!

3. Top 5 Forex Trading Mistakes Beginners Should Avoid

Know more!

Frequently Asked

Questions on Trade.com

It’s quick and easy. Just click ‘Open Account’, fill in your details, and upload your KYC documents (ID + proof of address). Once verified, you’re ready to fund and trade.

Start with as little as $100 for a Silver account. Want tighter spreads and premium features? Higher-tier accounts start from $10,000 (Gold) up to $100,000+ (Exclusive).

Absolutely. Trade.com is fully regulated across multiple jurisdictions. Your funds are held in segregated accounts and protected under strict financial standards.

Yes! With Trade.com, you can trade on-the-go using our mobile app, WebTrader, or MetaTrader 5 (MT5). Enjoy fast, secure, and seamless trading across all devices.

Access 850+ instruments including Forex, Stocks, Indices, ETFs, Commodities, and Cryptocurrencies. All under one platform — all commission-free.